Understand the Making Tax Digital (MTD) for Income Tax rules, thresholds, quarterly filing requirements and penalties with this practical guide from Northwyn Accounting & Advisory.

MTD Quarterly Updates: The Key Numbers

A practical reference guide covering the key thresholds, deadlines, reporting requirements and penalties for Making Tax Digital (MTD) for Income Tax.

This guide provides a summary of the current MTD for Income Tax rules. Individual circumstances may vary and taxpayers should consider professional advice where required.

Who’s affected

- £50,000 — qualifying income threshold for MTD for Income Tax from self-employment and/or UK property income (based on the relevant tax year)

- Qualifying income sources are combined, not assessed separately (e.g. £30k self-employment + £25k property = in scope)

- Some taxpayers are deferred until 2027

- Exemptions exist — some automatic, some must be claimed

- HMRC does not reliably notify everyone affected

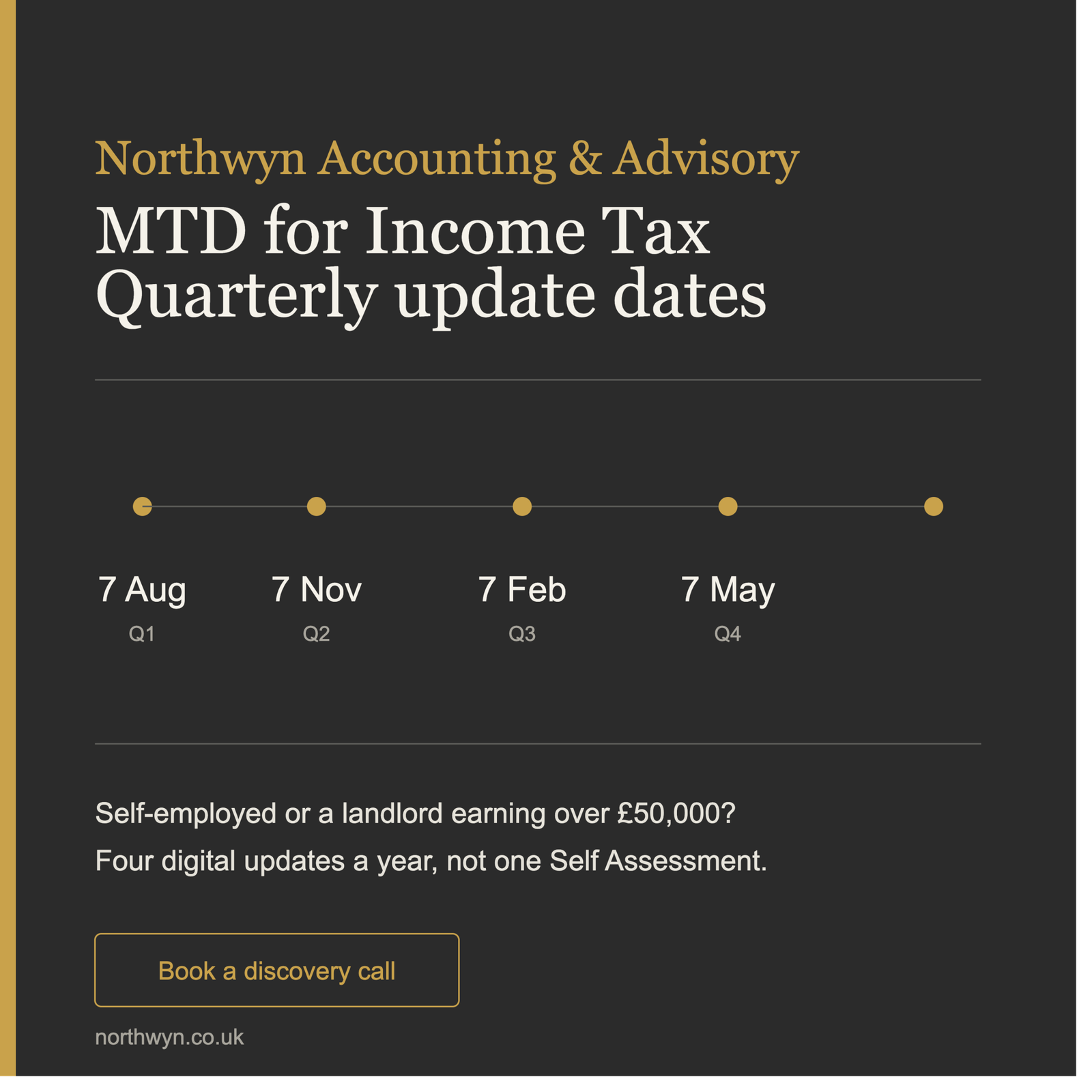

The four filing deadlines

| Deadline | Standard quarter covered |

|---|---|

| 7 August | 6 April – 5 July |

| 7 November | 6 April – 5 October |

| 7 February | 6 April – 5 January |

| 7 May | 6 April – 5 April |

- Updates are cumulative (year-to-date, not just the last 3 months)

- Can be filed up to 10 days early if no further transactions are expected

- Calendar quarter option available (1 April – 31 March) — but must be elected via software before your first update of the year, and isn’t supported by all software

What’s reported

- Self-employment: income and expenses across set categories (or simplified single totals if turnover is below the VAT registration threshold)

- UK property: income and expenses across set categories — residential property finance costs must always be reported separately, even under simplified reporting

- Foreign property: reported property-by-property

- Jointly-held property: income must be split by category in-year; expenses can be adjusted at year end instead

Penalties — late filing

- Points-based system

- 1 point per missed deadline (max 1 point per deadline, even with multiple income sources)

- 4 points = £200 penalty

- 0 penalty points for late filing in 2026/27 (soft landing year)

Penalties — late payment

Not covered by the soft landing — active from year one.

| Days late | Penalty |

|---|---|

| 15 days | 3% |

| 30 days | further 3% |

| 31+ days | 10% annual rate |

- Extra 15-day grace period in year one (30 days total before a penalty applies)

- Charged on top of standard late payment interest

- Does not apply to payments on account

In-year tax estimates

- Provided by HMRC after each quarterly update

- Based on the update plus other information HMRC already holds

- May not be accurate — not a substitute for your own figures

About Northwyn

Northwyn Accounting & Advisory helps landlords, sole traders and owner-managed businesses understand upcoming compliance changes and make informed tax decisions.

Unsure whether MTD for Income Tax applies to you or how to prepare? Northwyn can help you review your position, choose suitable software and stay compliant.

MTD for Income Tax

Making Tax Digital for Income Tax

MTD quarterly deadlines

MTD threshold

MTD penalties

MTD for landlords

MTD for sole traders